Budgets and forecasts

Budgets and forecasts are key to the success and growth of your business. A budget is a spending plan based on what you want to happen, while a forecast predicts what is likely to happen based on your past and present finances.

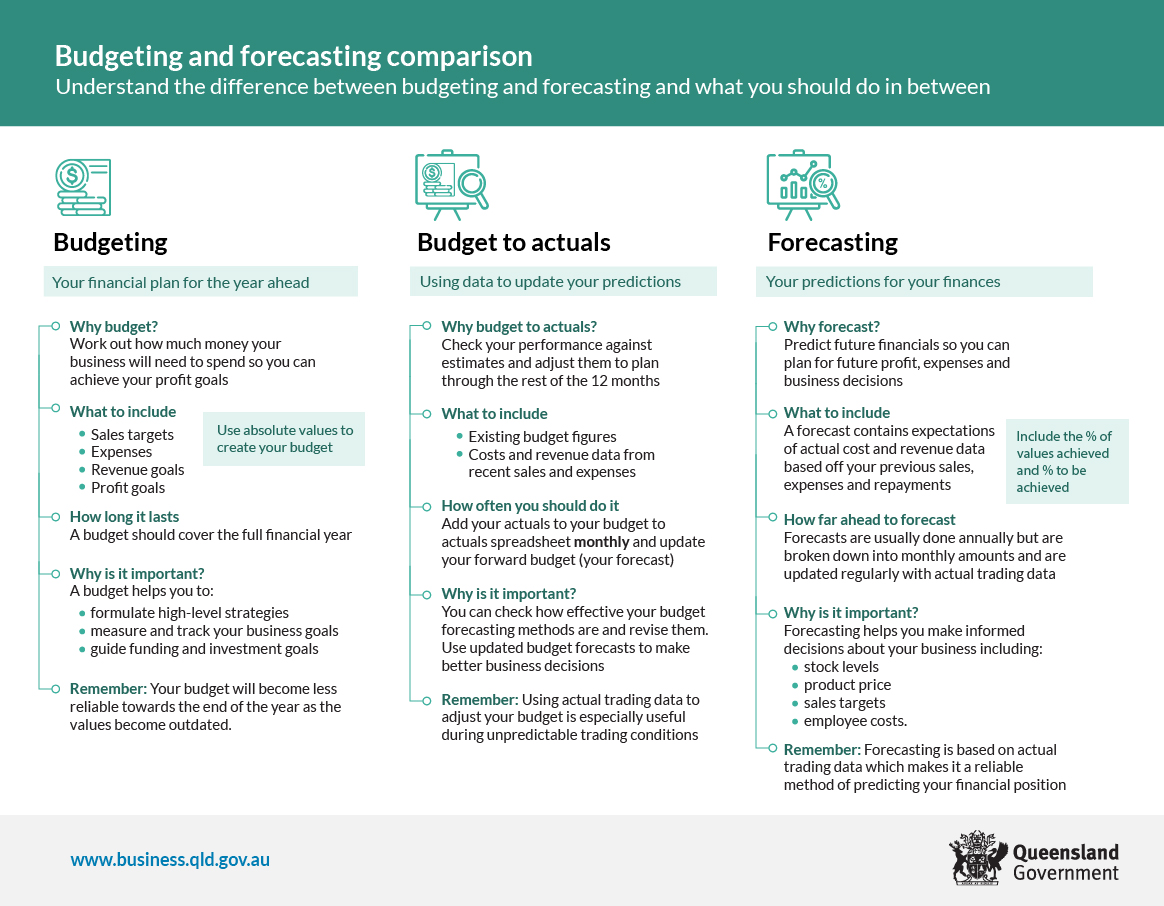

Budgeting and forecasting comparison

Budgeting and forecasting include:

- planning financially for the year ahead

- using data to update your predictions

- predicting future financials.

Use our budgeting and forecasting infographic (JPG, 442KB) to understand the differences between budgets and forecasts and when and why to use them.

Prepare a budget

Budgeting means outlining your expectations for the upcoming financial year. Budgets can estimate revenue, expenses and expected cash flows. They are generally updated annually and tend not to change over this time.

To set a budget, look at how much money your business spends, and how much money you can or should spend to maximise your profits.

If planned and managed well, a budget helps you to:

- monitor your sales and spending habits

- make better decisions and give you a competitive edge

- recognise how your decisions can impact business operations.

Your budget must be achievable. Work to a realistic budget that won't set you up to fail. When preparing your budget:

- use your existing financial statements to guide you

- review your business operating plan and note existing and new activities

- document assumptions such as cost of supplies (anticipating supply and demand considerations) and staffing costs

- consider working with your accountant, bookkeeper or tax agent for tailored advice.

Profit and loss budget

A profit and loss budget shows the expected revenue and expenses for your business over a period (usually 12 months) and will show if your business is running to plan. It calculates the sales targets needed to reach your profit goals.

A profit and loss budget:

- shows how much profit is likely from predicted sales

- contains non-cash items such as depreciation, creditors you have not paid, and invoices raised but for which no cash has been received

- excludes any payment of loans.

You can compile your profit and loss budget in the same format as your profit and loss statement. This will allow you to compare them later and refine future projections.

Prepare a forecast

Forecasts use actual sales and cost data to show where your finances are headed. It is an estimate of what your results and profitability will be. Forecasts are more dynamic than budgets, so update them regularly as your revenue and expenses change. It provides a basis for your financial decisions, using actual data for the financial year, and can be used to develop future budgets.

To create a forecast, use the data from your budget, along with previous and current business trends, to estimate what those profits will be.

Talk to your accountant or financial adviser for help to prepare a forecast and manage your forecasted cash flow. If you anticipate any cash shortfalls, you will need to plan how to cover your costs. These extra payments or receipts must be included in your cash flow forecast.

Review and update your forecasts at the end of each month when you compare your actual trading results with your original budgets (variance). You should then revise your forecasts for the rest of the financial year, considering where your business is heading. Your original budgets do not change.

If your business is facing uncertainty, you could create a range of forecasts based on different outcomes. This allows you to plan for every scenario and have a 'Plan B' and 'Plan C' if you don't achieve your ideal results.

Steps to prepare a forecast

-

Start by defining your forecast period. This could be monthly (most common), quarterly or yearly, depending on how your business handles billing. For example, if your business takes in daily sales from many different customers, create a monthly forecast. If you only bill a small number of clients quarterly, you may prefer a longer forecast period.

Base your future projections off past financial statements. There may be consistent monthly or yearly trends which allow you to accurately predict ongoing income. Adjust your forecast as trends change.

If your business is new and doesn't have a financial history, use your expected expenses. Work out how much your business is spending to know how much you need to earn to make a profit.

You may need to update your forecast throughout the period if your income fluctuates or expected sales figures change.

Remember to include all future cash inflows, even if they're not related to income or sales. This could include:

- if you are repaid a loan

- asset sales

- government grant payments.

-

Negative cash flow is money that is going out of your business (your expenses).

Expenses include everything from office supplies to staff salaries, administration, and fuel costs if your business owns a vehicle. Itemise your expenses as much as possible to help manage your forecast into the future.

Make sure you include other cash outflows beyond your ongoing monthly expenses. This could be the purchase of property or assets, or one-off payments.

-

Once you have an outline of your cash inflows and outflows, add the numbers into your forecast. You can do this as you're expense and income figures become available. Complete your projections and then add them to create your final document.

Once you've added your incoming and outgoing cash, you'll be able to estimate your closing cash balance for each period – this is the amount of cash you'll have left. This figure is then carried forward as your opening cash balance for the next period.

-

Once you've completed your cash flow forecast, you'll continue to use it throughout the period to review your actual cash flows against your original estimates. Review this regularly – weekly or fortnightly is recommended. Identify any differences and adjust your budget, business plan and expectations to improve your cash flow.

Review your results at the end of each month and compare these with your budget and forecast. Note any variances and keep track of whether these are either:

- a one-off occurrence (called a timing variance, where you may not have hit your targets this month but are likely to in future periods)

- for example, a contract end date has been unexpectedly delayed, meaning revenue will be generated later than anticipated

- an emerging permanent trend (called a permanent variance, where your estimates are unlikely to occur at all)

- for example, your business fails to win a contract, meaning you won't generate the revenue you forecasted.

Use this data to decide whether you need to adjust your cash flow forecasts or restructure your budget.

- a one-off occurrence (called a timing variance, where you may not have hit your targets this month but are likely to in future periods)

Cash flow forecast

A cash flow forecast is an estimate of how much money is likely to move in and out of your business over a period. It helps you predict cash surpluses or shortages and shows if your business has the cash it needs to keep running.

You can use a cash flow forecast to find out if you have sufficient available cash to pay your debts and taxes when they become due, or if you can afford to make a major equipment purchase, take on more staff or expand your business.

Set up your forecast in the same way as your cash flow statement to compare your predictions with your actual performance. This will alert you to any variances, which you can then investigate and find out why your business is under (or over) performing.

Cash flow forecasting is an estimate only, and your actual future income and expenses may vary from your original plan. You can limit these variances by being as accurate as possible when mapping out the timing of your incoming and outgoing expenses.

Use the following steps to help prepare a cash flow forecast.

You will need to estimate and record these amounts for each month.

- Total monthly cash inflow – includes sales, sales of assets, capital injections from borrowings or owners funds, interest revenue and any other sources.

- Total monthly cash outflow – includes items such as purchases, loan payments, supplies, telephone(s), electricity, wages and any other bills.

- Net cash flow – take the total outflows from the total inflows to see if there is more money in or out.

- Opening balance – record your cash available at the beginning of the month.

- Closing balance – calculate your funds available at the end of the month by adding the net cash flow to the opening balance. This will become your opening balance for the next month. Note: If your net cash flow is negative, this amount will be reduced.

Include GST when inserting amounts for some cash inflows (particularly sales) and many cash outflows (particularly purchases). Calculate the difference between total GST inflows and total GST outflows and insert this as GST payments.

Different GST requirements apply to different businesses. Seek specific advice from your tax adviser.

Also consider...

- Learn about other types of financial statements.

- Read about making your business more profitable.

- Learn about financial ratios to monitor your financial performance.

- Find out how to manage your cash flow.

- Find information, tips and resources on setting up and managing your business finances from our Mentoring for Growth mentors.